New Chapter 11 Filing - CTI Foods LLC

CTI Foods LLC

March 10, 2019

CTI Foods LLC, a large independent provider of “custom food solutions” to major hamburger, sandwich and Mexican restaurant chains…wait, stop. “Custom food solutions"? Seriously? Does everything need to be made to sound technological these days? Homies produce hamburgers, cooked sausage patties, grilled chicken, shredded beef and chicken, fajita meat, ham, Philly steak, dry sausage, beans, soups, macaroni & cheese, chili, sauces, and other sheet pan and retail meals through seven production facilities; they service QSRs and fast casual restaurants, including four of the top six hamburger restaurant chains, four of the top six sandwich chains, and “the top Mexican restaurant chain.” Queremos Taco Bell?!? Anyway, that’s basically it: let’s not over-complicate matters.

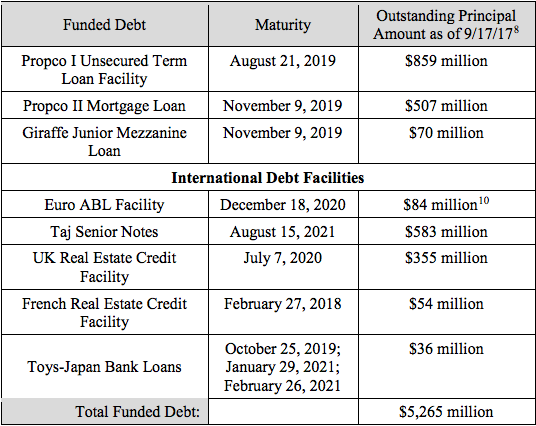

In any event, lenders must love custom food solutions because they’ve offered a solution of their own…to the company’s balance sheet. The company filed a prepackaged bankruptcy in the District of Delaware with substantial numbers of holders of first lien and second lien term loans hopping on board in support of the plan of reorganization (though not enough second lien term lenders to establish a fully consensual plan by bankruptcy thresholds). The filing is predicated upon accomplishing the results set forth in this handy-dandy chart:

Source: First Day Declaration

Pursuant to the plan, the first lien term lenders will receive some take-back paper and equity in the reorganized company, the second lenders will either equitize or cancel all $140mm of second lien term loan claims and existing equity will get wiped out. Trade creditors will ride through unimpaired. The company has secured a $155mm DIP commitment, the proceeds of which will be used, in part, to take out the ABL, and provide liquidity to fund the cases. Remaining funds will roll into an exit facility for the company to use post-emergence from bankruptcy. Just one thing: the chart shows a $50mm exit ABL and yet the company’s papers note a new $110mm exit ABL. Insert confusion here. 🤔

Confusion aside, this is a real business: the debtors apparently generated $1.2b of revenue in 2018 (and $29mm of EBITDA). Unfortunately, the private equity bros realized that back in 2013 when Thomas H. Lee Partners and Goldman Sachs & Co. acquired it from Littlejohn & Co. LLC. Per the company, the “current capital structure is the result of organic growth coupled with…strategic acquisitions….” So, uh, the capital structure didn’t fund the sponsor-to-sponsor purchase? Or is that “organic growth?” We suspect the former because, well, private equity, right? Debt is their jam. Oh, and the intercreditor agreement dated June 28, 2013 — mere months after the transaction — reflects that the debt was in place then rather than subsequently added to finance “organic growth.”* This is why PE firms pay firms like Weil the big bucks: first-class subterfuge. But…busted!

A quick aside, buried in paragraph 55 of the First Day Declaration is a cursory statement about the Restructuring Committee’s investigation into the company PE overlords. The company states:

On November 20, 2018, the Restructuring Committee separately retained Katten Muchin Rosenman LLP (“Katten”) as independent counsel. Specifically, the Restructuring Committee, with the assistance of Katten, conducted a thorough investigation into whether any potentially material claims or causes of action existed against directors, officers, or existing equity holders of the Debtors, including Goldman Sachs and T.H. Lee. Katten made extensive diligence requests to the Debtors, reviewed materials provided in response, interviewed several potential witnesses, and prepared a report for the Restructuring Committee evaluating the strengths and weaknesses of any such potential claims or causes of action. Ultimately, based on that investigation and the report prepared in connection therewith, the Restructuring Committee determined it was unlikely that any such meritorious claims or causes of action exist that ought to be pursued.

It’s a good thing trade is riding through: there likely won’t be an official committee of unsecured creditors to test this conclusion.

So, aside from the company-crushing transaction-induced debt placed on the company by its private equity overlords, why is the company in bankruptcy? Here’s where you really need to read between the lines: above we noted that the company “service[s] QSRs and fast casual restaurants, including four of the top six hamburger restaurant chains, four of the top six sandwich chains, and ‘the top Mexican restaurant chain.’” “Service” is the key word. We don’t see the word “exclusively” preceding it. Here’s the company:

CTI’s recent profitability decline is attributable in part to an increase in the number of protein processors in competitive segments of the food manufacturing and foodservice industries, which led to losses in customer shares and a decrease in new business for the Company. Simultaneously … the Company’s costs have increased over time. The combination of increased competition and increased costs resulted in lower volumes and narrower profit margins. (emphasis added)

Costs increased for a number of reasons — integration of new facilities, etc. — but the most disturbing one is food quality control. Per the company:

The Company’s profitability also suffered from food quality incidents in 2017 and 2018. Although the Company quickly identified and remedied the issues, those occurrences led to a loss of customer sales and to the incurrence of significant costs in remedying the situation and ensuring the integrity of products manufactured on a go-forward basis. These costs, albeit temporary, have collectively had a material impact on the Company’s recent profitability levels.

Yikes. That’s no bueno.

Now, there is some good news here. First, the company appears to have improved EBITDA in Q4 ‘18. Second, this plan is mostly consensual. And, third, the prepackaged nature of this plan will help the company accomplish their restructuring in a speedy six weeks, as planned. Food safety depends on it.

*$25mm of the principal amount of first lien term loans outstanding is attributable to a 2016 acquisition. To be fair.

Jurisdiction: D. of Delaware (Judge Sontchi)

Capital Structure: see above.

Company Professionals:

Legal: Weil Gotshal & Manges LLP (Matthew Barr, Ronit Berkovich, Lauren Tauro, Clifford Carlson, David Li, Michael Godbe) & (local) Young Conaway Stargatt & Taylor LLP (M. Blake Cleary, Jaime Luton Chapman, Shane Reil)

Legal to Restructuring Committee: Katten Muchin Rosenman LLP

Financial Advisor/CRO: AlixPartners LLP (Kent Percy)

Investment Banker: Centerview Partners LLC (Karn Chopra)

Claims Agent: Prime Clerk LLC (*click on company name above for free docket access)

Other Parties in Interest:

Prepetition Credit Agreement Agent: Wells Fargo Bank NA

Legal: Otterbourg PC (Andrew Kramer) & (local) Richards Layton & Finger PA (Mark Collins, Jason Madron)

Ad Hoc Group of Term Lenders & DIP Term Agent ($155mm): Cortland Capital Market Services LLC

Legal: Davis Polk & Wardwell LLP (Damian Schaible, Michelle McGreal, Stephen Piraino) & (local) Morris Nichols Arsht & Tunnell LLP (Robert Dehney, Curtis Miller, Matthew Harvey)

ABL DIP & Exit Agent ($235mm): Barclays Bank PC

Legal: Sherman & Sterling LLP (Joel Moss, Jordan Wishnew) & (local) Richards Layton & Finger PA (Mark Collins, Jason Madron)