👕 New Chapter 11 Bankruptcy Filing - Chinos Holdings Inc. (J.Crew) 👕

Chinos Holdings Inc. (J.Crew)

May 4, 2020

If you’re looking for a snapshot of the pre-trade war and pre-COVID US economy look no farther than J.Crew’s list of top 30 unsecured creditors attached to its chapter 11 bankruptcy petition. On the one hand there is the LONG list of sourcers, manufacturers and other middlemen who form the crux of J.Crew’s sh*tty product line: this includes, among others, 12 Hong Kong-based, three India-based, three South Korea-based, two Taiwan-based, and two Vietnam-based companies. In total, 87% of their product is sourced in Asia (45% from mainland China and 16% from Vietnam). On the other hand, there are the US-based companies. There’s Deloitte Consulting — owed a vicious $22.7mm — the poster child here for the services-dependent US economy. There’s the United Parcel Services Inc. ($UPS)…okay, whatever. You’ve gotta ship product. We get that. And then there’s Wilmington Savings Fund Society FSB, as the debtors’ pre-petition term loan agent, and Eaton Vance Management as a debtholder and litigant. Because nothing says the US-of-f*cking-A like debt and debtholder driven litigation. ‘Merica! F*ck Yeah!!

Chinos Holdings Inc. (aka J.Crew) and seventeen affiliated debtors (the “debtors”) filed for bankruptcy early Monday morning with a prearranged deal that is dramatically different from the deal the debtors (and especially the lenders) thought they had at the tail end of 2019. That’s right: while the debtors have obviously had fundamental issues for years, it was on the brink of a transaction that would have kept it out of court. Call it “The Petsmart Effect.” (PETITION Note: long story but after some savage asset-stripping the Chewy IPO basically dug out Petsmart from underneath its massive debt load; J.Crew’s ‘19 deal intended to do the same by separating out the various businesses from the Chino’s holding company and using Madewell IPO proceeds to fund payments to lenders).

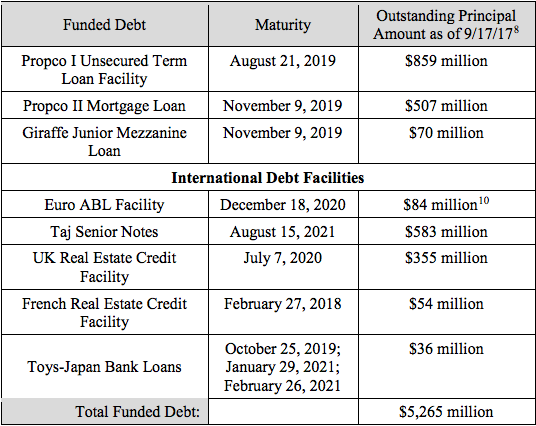

Here is the debtors’ capital structure. It is key to understanding what (i) the 2019 deal was supposed to accomplish and (ii) the ownership of J.Crew will look like going forward:

Late last year, the debtors and their lenders entered into a Transaction Support Agreement (“TSA”) with certain pre-petition lenders and their equity sponsors, TPG Capital LP and Leonard Green & Partners LP, that would have (a) swapped the $1.33b of term loans for $420mm of new term loans + cash and (b) left general unsecured creditors unimpaired (100% recovery of amounts owed). As noted above, the cash needed to make (a) and (b) happen would have come from a much-ballyhooed IPO of Madewell Inc.

Then COVID-19 happened.

Suffice it to say, IPO’ing a brick-and-mortar based retailer — even if there were any kind of IPO window — is a tall order when there’s, like, a pandemic shutting down all brick-and-mortar business. Indeed, the debtors indicate that they expect a $900mm revenue decline due to COVID. That’s the equivalent of taking Madewell — which earned $602m of revenue in ‘19 after $614mm in ‘18 — and blowing it to smithereens. Only then to go back and blow up the remnants a second time for good measure.* Source of funds exit stage left!

The post-COVID deal is obviously much different. The term lenders aren’t getting a paydown from Madewell proceeds any longer; rather, they are effectively getting Madewell itself by converting their term loan claims and secured note claims into approximately 82% of the reorganized equity. Some other highlights:

Those term loan holders who are members of the Ad Hoc Committee will backstop a $400mm DIP credit facility (50% minimum commitment) that will convert into $400mm of new term loans post-effective date. The entire plan is premised upon a $1.75b enterprise value which is…uh…interesting. Is it modest considering it represents a $1b haircut off the original take-private enterprise value nine years ago? Or is it ambitious considering the company’s obvious struggles, its limited brand equity, the recession, brick-and-mortar’s continued decline, Madewell’s deceleration, and so forth and so on? Time will tell.

Syndication of the DIP will be available to holders of term loans and IPCo Notes (more on these below), provided, however, that they are accredited institutional investors.

The extra juice for putting in for a DIP allocation is that, again, they convert to new term loans and, for their trouble, lenders of the new term loans will get 15% additional reorganized equity plus warrants. So an institution that’s in it to win it and has a full-on crush for Madewell (and the ghost of JCrew-past) will get a substantial chunk of the post-reorg equity (subject to dilution).

Query whether, if asked a mere six months ago, they were interested in owning this enterprise, the term lenders would’ve said ‘yes.’ Call us crazy but we suspect not. 😎

General unsecured creditors’ new deal ain’t so hot in comparison either. They went from being unimpaired to getting a $50mm pool with a 50% cap on claims. That is to say, maybe…maybe…they’ll get 50 cents on the dollar.

That is, unless they’re one of the debtors’ 140 landlords owed, in the aggregate, approximately $23mm in monthly lease obligations.** The debtors propose to treat them differently from other unsecured creditors and give them a “death trap” option: if they accept the TSA’s terms and get access to a $3mm pool or reject and get only $1mm with a 50% cap on claims. We can’t imagine this will sit well. We imagine that the debtors choice of venue selection has something to do with this proposed course of action. 🤔

We’re not going to get into the asset stripping transaction at the heart of the IPCo Note issuance. This has been widely-covered (and litigated) but we suspect it may get a new breath of life here (only to be squashed again, more likely than not). In anticipation thereof, the debtors have appointed special committees to investigate the validity of any claims related to the transaction. They may want to take up any dividends to their sponsors while they’re at it.

The debtors hope to have this deal wrapped up in a bow within 130 days. We cannot even imagine what the retail landscape will look like that far from now but, suffice it to say, the ratings agencies aren’t exactly painting a calming picture.

*****

*Curiously, there are some discrepancies here in the numbers. In the first day papers, the debtors indicate that 2018 revenue for Madewell was $529.2mm. With $602mm in ‘19 revenue, one certainly walks away with the picture that Madewell is a source of growth (13.8%) while the J.Crew side of the business continues to decline (-4%). This graph is included in the First Day Declaration:

Source: First Day Declaration

The Madewell S-1, however, indicates that 2018 revenue was $614mm.

With $268mm of the ‘18 revenue coming in the first half, this would imply that second half ‘18 revenue was $346mm. With ‘19 revenue coming in at $602mm and $333mm attributable to 1H, this would indicate that the business is declining rather than growing. In the second half, in particular, revenue for fiscal ‘19 was $269mm, a precipitous dropoff from $333mm in ‘18. Even if you take the full year fiscal year ‘18 numbers from the first day declaration (529.2 - 268) you get $261mm of second half growth in ‘18 compared to the $269mm in ‘19. While this would reflect some growth, it doesn’t exactly move the needle. This is cause for concern.

**To make matters worse for landlords, the debtors are also seeking authority to shirk post-petition rent obligations for 60 days while they evaluate whether to shed their leases. We get that the debtors were nearing a deal that COVID threw into flux, but this bit is puzzling: “Beginning in early April 2020, after several weeks of government mandated store closures and uncertainty as to the duration and resulting impact of the pandemic, the Debtors began to evaluate their lease portfolio to, among other things, quantify and realize the potential for lease savings.” Beginning in early April!?!?

Jurisdiction: E.D. of Virginia (Judge )

Capital Structure: $311mm ABL (Bank of America NA), $1.34b ‘21 term loan (Wilmington Savings Fund Society FSB), $347.6 IPCo Notes (U.S. Bank NA)

Professionals:

Legal: Weil Gotshal & Manges LLP (Ray Schrock, Ryan Preston Dahl, Candace Arthur, Daniel Gwen) & Hunton Andrews Kurth LLP (Tyler Brown, Henry P Long III, Nathan Kramer)

JCrew Opco Special Committee: D.J. (Jan) Baker, Chat Leat, Richard Feintuch, Seth Farbman

Financial Advisor: AlixPartners LLP

Investment Banker: Lazard Freres & Co.

Real Estate Advisor: Hilco Real Estate LLC

Claims Agent: Omni Agent Solutions (*click on the link above for free docket access)

Other Parties in Interest:

Pre-petition ABL Agent: Bank of America NA

Legal: Choate Hall & Stewart LLP (Kevin Simard, G. Mark Edgarton) & McGuireWoods LLP (Douglas Foley, Sarah Boehm)

Pre-petition Term Loan & DIP Agent ($400mm): Wilmington Savings Fund Society FSB

Legal: Seward & Kissel LLP

Ad Hoc Committee

Legal: Milbank LLP (Dennis Dunne, Samuel Khalil, Andrew LeBlanc, Matthew Brod) & Tavenner & Beran PLC (Lynn Tavenner, Paula Beran, David Tabakin)

Financial Advisor: PJT Partners Inc.

Large common and Series B preferred stock holders: TPG Capital LP (55% and 66.2%) & Leonard Green & Partners LP (20.7% and 24.8%)

Legal: Paul Weiss Rifkind Wharton & Garrison LLP (Paul Basta, Jacob Adlerstein, Eugene Park, Irene Blumberg) & Whiteford Taylor & Preston LLP (Christopher Jones, Vernon Inge Jr., Corey Booker)

Large Series A preferred stock holders: Anchorage Capital Group LLC (25.6%), GSO Capital Partners LP (26.1%), Goldman Sachs & Co. LLC (15.5%)