11/29/17 Recap: It has become routine for a company to tout the synergistic benefits of an acquisition. But synergies only come from solid execution and integration of the new properties into the existing franchise. As we often see, that's a pipe dream that often fails to come to fruition. Take, Cumulus Media, for instance, which from 1998 through 2013, "completed approximately $5 billion worth of acquisitions to grow its network and station businesses," including two large recent acquisitions (Citadel Broadcasting in 2011 and Westwood One in 2013). Notably, "[t]he Company struggled to develop the management and technology infrastructure required to integrate the acquired assets and to support and manage its expanding portfolio. Additionally, certain of the acquisition projections proved erroneous and a number of subsequent management decisions failed to achieve their desired results. The Company was thus unable to achieve the cash flow projections it had made to support the prices paid for those acquisitions...." Projections didn't translate to reality? Color us shocked. Combine these operational challenges with "industry challenges" and you've got a recipe for decreased YOY trends in ratings, revenue and EBITDA. Since 2012. Yikes. But like most bankruptcies, this is a storm of multiple elements. Clearly, the above-noted transactions led to a tremendous amount of incurred debt, capex for integration, and interest expense on that debt. But, in addition, "advertiser and listener demand for radio overall has been negatively impacted by the availability of content and advertising opportunities in growing digital streaming and web-based digital formats, resulting in declines in radio industry revenue and listenership. As a result of these general industry pressures, high acquisition prices and subsequent poor performance, Cumulus Media found itself with an excessive level of debt relative to its earnings and rapidly approaching maturities on its funded debt." So, in other words, blame the debt, Facebook ($FB), Google ($GOOGL), Netflix ($NFLX), Amazon ($AMZN), podcasts, etc., for the decline in radio consumption. So, now the company is in bankruptcy with a restructuring support agreement in place to equitize the term loan. The term loan lenders will get take-back paper and 83.5% percent of the reorganized company. The noteholders will get 16.5% of the equity subject to management incentive plan. Shareholders will get bupkis.

Jurisdiction: S.D. of New York (Judge Chapman)

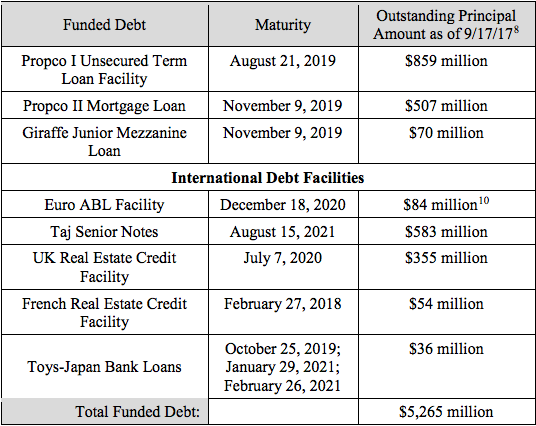

Capital Structure: $1.73b TL (JP Morgan Chase Bank NA), $637mm 7.75% senior notes (U.S. Bank NA)

Company Professionals:

Legal: Paul Weiss Rifkind Wharton & Garrison LLP (Paul Basta, Lewis Clayton, Jacob Adlerstein, Claudia Tobler)

Financial Advisor: Alvarez & Marsal North America LLC (David Miller)

Investment Banker: PJT Partners LP

Claims Agent: Epiq Bankruptcy Solutions LLC (*click on company name above for free docket access)

Board of Directors: Mary Berner, Jill Bright, Ralph Everett, Jeffrey Marcus, Ross Oliver, Jan Baker

Other Parties in Interest:

Ad Hoc Group of Term Loan Lenders (Eaton Vance Management and Boston Management & Research, Franklin Mutual Advisors, Highland Capital Management LP, JP Morgan Chase Bank NA, Silver Point Finance LLC, Symphony Asset Management LLC and Nuveen Fund Advisors, Voya Investment Management Co. LLC, Beach Point Capital Management LP)

Legal: Arnold & Porter Kaye Scholer LLP (Michael Messersmith, Michael Solow, Seth Kleinman)

Financial Advisor: FTI Consulting LLC

Ad Hoc Senior Noteholder Group (Angelo Gordon & Co. LLP, Brigade Capital Management, Capital Research and Management Co., Greywolf Capital Management LP, Waddell & Reed Investment Corporation)

9/19/17 Recap: So. Much. To. Unpack. Here. We've previously discussed the run-up to this massive chapter 11 bankruptcy filing here and here. Still, suffice it to say that, unlike many of the other retailers that have predictably filed for bankruptcy thus far in 2017, this one was different. This one seemingly came out of nowhere - particularly given the proximity to the holiday shopping season. Before we note what this case is, lets briefly cover what it isn't and clear the noise that is pervasive on the likes of Twitter: this is NOT "RIP" Toys "R" Us. We don't get overly sentimental usually but the papers filed with the bankruptcy court were well-written and touching: this is a store, a brand, that means a lot to a lot of people. And it's not going anywhere (the company will have its challenges to assure people that this is the case). This is a financial restructuring not a liquidation: the company simply hasn't been able to evolve while paying $400mm in annual interest expense on over $5b of private equity infused debt. Plain and simple. Yes, there are other challenges (blah blah blah, Amazon), but with that debt overhang, it appears the company hasn't been able to confront them (PETITION side note: an ill-conceived deal with Amazon 18 years ago is mind-blowing when viewed from the perspective of Amazon's long game). With this filing, the company is signaling that the time for short term band-aids to address its capital structure is over. Now, "[t]he time for change, and reinvestment in operations, has come." Decisive. Management isn't messing around anymore. With a reduction in debt, the company will be unshackled and able to focus on "general upkeep and the condition of...stores, [its] inability to provide expedited shipping options, and [its] lack of a subscription-based delivery service." Indeed, the company intends to use a $3.1b debtor-in-possession credit facility to begin investing in modernization immediately.

Interesting Facts:

Toy Manufacturers: Mattel ($MAT)(approx $136mm), Hasbro ($HAB) (approx $59mm) & Lego (approx $31.5mm) are among the top general unsecured creditors of the company. Mattel and Hasbro's stock traded down quite a bit yesterday on the rampant news of this filing. Query whether any of the $325mm of requested critical vendor money will apply to these companies.

The Power of the Media (read: NOT "fake news"): This CNBC piece helped push the company into bankruptcy. Bankruptcy professionals were retained in July (or earlier in the case of Lazard) to pursue capital structure solutions. In August the company engaged with some of its lenders. But then "...a news story published on September 6, 2017, reporting that the Debtors were considering a chapter 11 filing, started a dangerous game of dominos: within a week of its publication, nearly 40 percent of the Company’s domestic and international product vendors refused to ship product without cash on delivery, cash in advance, or, in some cases, payment of all outstanding obligations. Further, many of the credit insurers and factoring parties that support critical Toys “R” Us vendors withdrew support. Given the Company’s historic average of 60-day trade terms, payment of cash on delivery would require the Debtors to immediately obtain a significant amount—over $1.0 billion—of new liquidity."

Revenue. The company generates 40% of its annual revenue during the holiday season.

Footprint. The company has approximately 1,697 stores and 257 licensed stores in 38 countries, plus additional e-commerce sites in various countries. The company has been shedding burdensome above-market leases and combining its Babies and Toys shops under one roof; it intends to continue its review of its real estate portfolio. Read: there WILL be store closures.

Eff the Competition. Toys has some choice words for its competition embedded in its bankruptcy papers; it accuses Walmart ($WMT) and Target ($TGT)(the "big box retailers") of slashing prices on toys and using toys as a loss leader to get bodies in doors; it further notes that "retailers such as Amazon are not concerned with making a profit at this juncture, rendering their pricing model impossible to compete with..." ($AMZN). Yikes.

Experiential Retail. The company intends to invest in the "shopping experience" which will include (i) interactive spaces with rooms to use for parties, (ii) live product demonstrations put on by trained employees, and (iii) the freedom for employees to remove product from boxes to let kids play with the latest toys. And...wait for it...AUGMENTED REALITY. Boom. Toysrus.ar and Toysrus.ai here we come.

Jurisdiction: E.D. of Virginia (Judge Phillips)

Capital Structure: see below

Company Professionals:

Legal: Kirkland & Ellis LLP (Jamie Sprayragen, Anup Sathy, Edward Sassower, Chad Husnick, Joshua Sussberg, Robert Britton, Emily Geier) & (local) Kutak Rock LLP (Michael A. Condyles, Peter J. Barrett, Jeremy S. Williams) & (Canadian counsel) Goodmans LLP

Legal to the Independent Board of Directors: Munger, Tolles & Olson LLP

Financial Advisor: Alvarez & Marsal North America LLC (Jeffrey Stegenga, Jonathan Goulding, Tom Behnke, Cari Turner, Jim Grover, Arjun Lal, Doug Lewandowski, Bobby Hoernschemeyer, Scott Safron, Kara Harmon, Nick Cherry, Adam Fialkowski)

Real Estate Consultant: A&G Realty Partners LLC (Andrew Graiser)

Claims Agent: Prime Clerk LLC (*click on company name above for free docket access)

Communications Consultant: Joele Frank Wilkinson Brimmer Katcher

Other Parties in Interest:

ABL/FILO DIP Admin Agent: JPMorgan Chase Bank NA

Legal: Davis Polk & Wardwell LLP (Marshall Heubner, Brian Resnick, Eli Vonnegut, Veerle Roovers) & (local) Hunton & Williams LLP (Tyler Brown, Henry (Toby) Long III, Justin Paget)

DIP Admin Agent (Toys DE Inc). NexBank SSB & Ad Hoc Group of B-4 Lenders (Angelo Gordon & Co LP; Franklin Mutual Advisors LLC, HPS Investment Partners LLC, Marathon Asset Management LP, Redwood Capital Management LLC, Roystone Capital Management LP, and Solus Alternative Asset Management LP)

Legal: Wachtell Lipton Rosen & Katz (Joshua Feltman, Emil Kleinhaus, Neil Chatani) & (local) McGuireWoods LLP (Dion Hayes, Sarah Bohm, Douglas Foley)

Ad Hoc Group of Taj Noteholders.

Legal: Paul Weiss Rifkind Wharton & Garrison LLP (Brian Hermann, Samuel Lovett, Kellie Cairns) & (local) Whiteford Taylor & Preston LLP (Christopher Jones, Jennifer Wuebker)

Steering Committee of B-2 and B-3 Lenders (American Money Management, Columbia Threadneedle Investments, Ellington Management Group LLC, First Trust Advisors L.P., MJX Asset Management LLC, Pacific Coast Bankers Bank, Par-Four Investment Management LLC, Sound Point Capital Management, Taconic Capital Advisors LP).

Legal: Arnold & Porter Kaye Scholer LLP (Michael Messersmith, D. Tyler Nurnberg, Sarah Gryll, Rosa Evergreen)

Committee of Unsecured Creditors (Mattel Inc., Evenflo Company Inc., Simon Property Group, Euler Hermes North America Insurance Co., Veritiv Operating Company, Huffy Corporation, KIMCO Realty, The Bank of New York Mellon, LEGO Systems Inc.)