😷New Chapter 11 Bankruptcy Filing - Quorum Health Corporation😷

Quorum Health Corporation

April 7, 2020

Tennessee-based Quorum Health Corporation, an operator of general acute care hospitals and outpatient healthcare facilities, filed for bankruptcy in the District of Delaware (along with a long list of affiliates). COVID-19!! Not quite. This turd has been circling around the chapter 11 bankruptcy bin for years now. The fact that it is only now filing for bankruptcy under the cloud of COVID simply serves as cover for its fundamentally unsound capital structure, its lack of integration post-spinoff and the composition of its patient base (rural and dependent upon Medicare and Medicaid). Your Nana’s acute care powered by private equity/Wall Street!

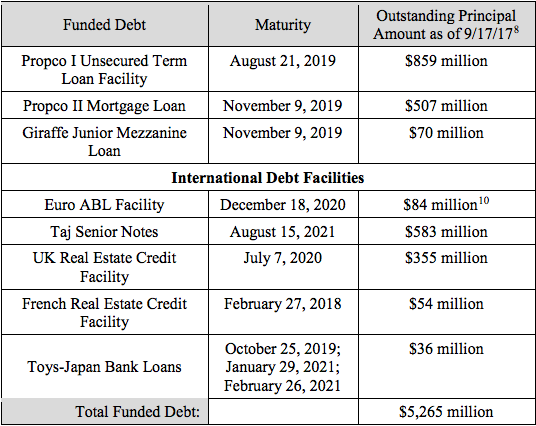

About that capital structure…we’re talking: $99mm ABL + $47mm RCF + $785.3mm in first lien loans and $400mm of senior notes for a solid total of ~$1.285b in funded debt. All of this debt was placed in connection with the debtors’ origin story: a 2015 spinoff from Community Health Systems Inc. ($CYH). Troubles began from there. The company states:

The assets the Company received in the Spin-off were not initially set up as an integrated, stand-alone enterprise and presented certain day-one integration challenges, including addressing significant geographic dispersion that resulted in a lack of scale in key markets. In addition, certain of the hospitals that the Company received in the Spin-off were underperforming….

If you’re wondering whether this spin-off might lead to fraudulent conveyance claims well, to (mis)quote Elizabeth Warren, the company’s plan of reorganization has a Trust for that. That ought to be fun.

Otherwise, this is a deleveraging transaction. The ABL and holders of first lien claims will come out whole. Likewise, general unsecured claims will ride through. The holders of the senior notes will equitize their claims and come out, prior to dilution, with 100% of the post-reorg equity. Certain lenders will write a $200mm equity check. The case is on a quick one-month timeline through which it will be funded by a $100mm DIP; therefore, come May, this hospital system will, hopefully, be ready to confront a post-COVID-19 world.

Jurisdiction: D. of Delaware (Judge Owens)

Capital Structure: ABL (UBS AG), RCF and Term Loan (Credit Suisse AG), $421.8mm ‘23 11.625% Senior Notes (Wilmington Savings Funds Society)

Professionals:

Legal: McDermott Will & Emery LLP (Felicia Perlman, Bradley Giordano, David Hurst, Megan Preusker)

Financial Advisor/CRO: Alvarez & Marsal (Paul Rundell, Steve Kotarba, David Blanks, Douglas Stout

Investment Banker: MTS Health Partners LP

Claims Agent: Epiq (*click on the link above for free docket access)

Other Parties in Interest:

DIP Agent: GLAS USA LLC

Consenting First Lien Lenders

Legal: Milbank LLP (Dennis Dunne, Tyson Lomazow)

Financial Advisor: Houlihan Lokey

Consenting Noteholders

Legal: Kirkland & Ellis LLP (Nicole Greenblatt, Steven Serajeddini)

Financial Advisor: Jefferies LLC

Major Shareholders: Mudrick Capital Management, LP, KKR & Co. Inc., York Capital Management Global Advisors LLC, Davidson Kempner Capital Management LP, and The Goldman Sachs Group Inc.