Is New York City F*cked?

Uber, Lyft, and Political Incompetence: Mayor de Blasio Needs to Get it Together

Maybe New York City Mayor Bill de Blasio ought to subscribe to PETITION. He clearly doesn’t grasp disruption. And other elected officials are calling him out on it.

Just recently, Thomas DiNapoli, State Comptroller, released his “Review of the Financial Plan of the City of New York”. Buried within the document is a subtle rebuke of the de Blasio administration’s failure to acknowledge any semblance of reality. Here are some key highlights:

- The November (Financial) Plan covers a four-year financial plan from 2018–2021. That plan projects a budget gap of $7.1b, a number dismissed as “relatively small as a share of City fund revenues (averaging 3.5 percent).” The gap has tightened in large part due to pension fund over-performance. PETITION Note: Hmmm. Query how long that will last.

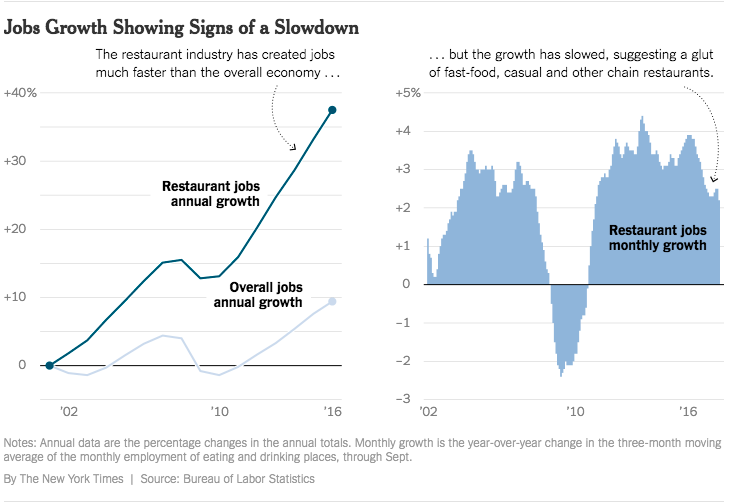

- NYC’s economy has expanded more than at any time since WWII. But job growth is slowing and may slow more given federal tax policies.

- The FY 2019 budget gap estimate was increased by $360mm to $4.4b because “tax receipts have fallen short of expectations.” “Despite the strength of the City’s economy, non-property tax collections have underperformed. For example, the City had assumed that business tax collections would increase by 9.1 percent in FY 2018, but collections declined instead by 8.9 percent during the first four months of the fiscal year (after declining for two consecutive years). Although the City lowered its forecast by $240 million in FY 2018, the out-year forecasts were left unchanged.” PETITION Note: read that last line again!

- The Plan anticipates $8.3b of federal funding in FY 2018, accounting for 10% of the City budget. PETITION Note: Right. We’ll see. There is obviously a real question whether the federal government may be counted on to fund the City at the same levels. And federal taxes and home ownership costs are obviously expected to increase for many City residents. “Changes in federal fiscal policies, however, constitute the greatest risk to the City since the Great Recession.”

And then our favorite bit:

- The City has 1650 taxi medallions to sell but has postponed sales since 2014 with the express acknowledgement that ride-sharing companies like Lyft and Uber are affecting medallion values. “The average sale price for a taxi medallion peaked at $1 million in calendar year 2014, but it was nearly cut in half by 2016. Weakness in market conditions has continued, with the average sale price declining in 2017 to $350,000 as of November 2017.” And, YET, the November Plan assumes the 1650 medallions will be sold at an average price of $728k.

Wait, what? Just last week, First Jersey Credit Union reportedly auctioned off six NYC taxi medallions for a high bid of $186k. And then on Tuesday January 16, five medallions were sold for a total of $875,000. Two additional medallions sold for $189k and $199k, respectively. To quote the previously linked Crain’s New York piece, “When a taxi medallion sold for $241,000 last March, the seemingly rock-bottom price made major news. It turns out, those were the good old days.” And then there is this, “One industry veteran said the auction prices are low, relatively speaking, because these are cash deals at a time when banks are not lending for medallion purchases.” Right, because the banks know that medallions make for crappy collateral and have zero desire to try and catch those falling knives. These are just the latest in a recent trend of distressed medallion sales — many of which have taken place in the bankruptcy courts. This stuff is public information. We’d think that Mayor de Blasio and his administration would be aware of it. Apparently not.

Here’s the problem: either through ignorance (it’s not like others haven’t noticed) or wishful thinking (that, what, Uber AND Lyft will FAIL?), the administration is budgeting on the basis of medallion sales that may never happen. And, even if they do, they are unlikely to fetch the value projected. Per DiNapoli, this error leaves an estimated $731mm shortfall in the budget. This is an astounding level of cluelessness. Even for a politician.

More importantly, if the de Blasio administration can’t see what is occurring right in front of them, how is it to be counted on to address bigger issues coming soon? Like autonomous cars, for instance? “‘Autonomous vehicles will have a significant and fundamental effect on cities and how they’re laid out’”. Color us concerned. If you live in New York, you should be too.