⚡️Update: CBL & Associates Properties Inc.⚡️

In our recent newsletter, “🇺🇸Forever 21: Living the (American) Dream🇺🇸,” we highlighted the exposure that landlords have to Forever21:

The company currently spends $450mm in annual rent, spread across 12.2mm total square feet. The company will close 178 stores in the US and 350 in total.

We highlighted how the company noted the impact this plan will have on large mall landlords, the company said:

Forever 21’s management team and its advisors worked with its largest landlords to right size its geographic footprint. Four landlords hold almost 50 percent of its lease portfolio. To date, Forever 21 and its landlords have engaged in productive negotiations but have not yet reached a resolution.

Two of those landlords were the largest unsecured creditors, Simon Property Group ($SPG) and Brookfield Property Partners ($BPY). But another, CBL & Associates Properties Inc. ($CBL), also has exposure. In “Thanos Snaps, Retail Disappears,” we discussed CBL’s issues: bankruptcy-related store closures are something that CBL is very familiar with. Management said last February that things were going to turn around but, instead, things just keep getting worse as more and more retailers go out of business.

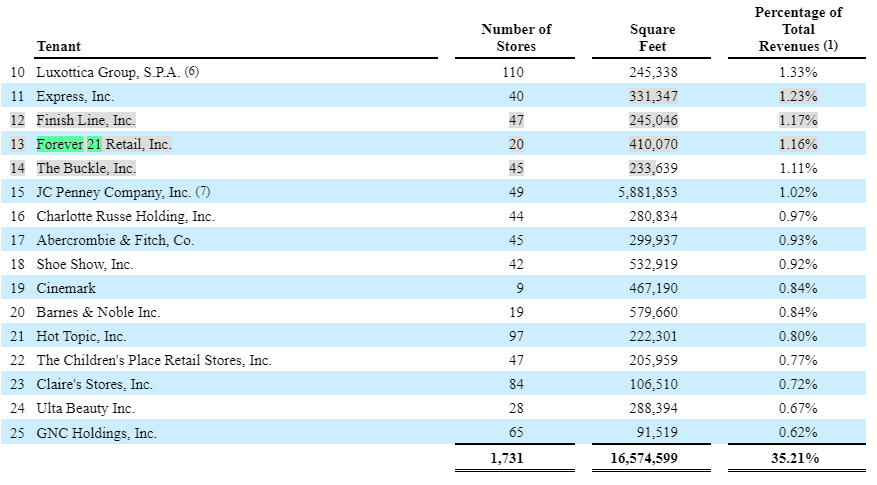

Forever 21 is one of CBL’s top tenants, occupying 19 stores (plus 1 store in “redevelopment phase”). Per CBL’s FY 2018 10-K, Forever 21 accounts for roughly 1.2% of CBL’s revenue or $10 million.

Of those 20 stores, 7 are subsumed by a motion by Forever 21 to enter into a consulting agreement to close stores (see bankruptcy docket (#81 Exhibit A):

On October 14, 2019, partly due Forever 21’s bankruptcy, Moody’s downgraded CBL’s corporate family rating to B2 from Baa3 and revised its outlook to negative. Moody’s explained:

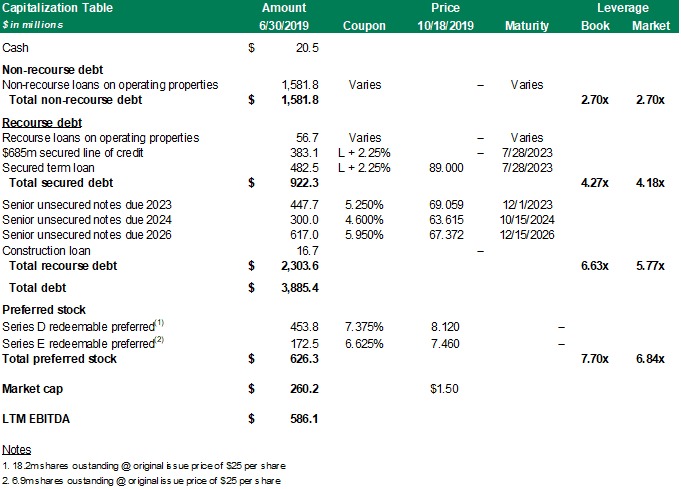

CBL's cushion on its bond covenant compliance is modest, particularly the debt service test, which requires consolidated income to debt service to annual debt service charge to be greater than 1.50x. The ratio has declined from 2.46x at year-end 2018 to 2.27x at Q1 2019, and 2.25x at Q2 2019 due principally to declining operating income during these periods. CBL's same-center NOI growth was -5.3% for Q2 2019 YTD and CBL projected same-center NOI growth to be between -7.75% and -6.25% for 2019, which means that the debt service test will likely weaken further.

The chart below reflects the company’s capital structure and debt prices. It is not doing well. In fact, the term loan and the unsecured notes have priced down considerably since March:

Here is the company's stock performance:

The last thing CBL needed — on the heals of the downgrade — was near-instantaneous bad news. It got it this week.

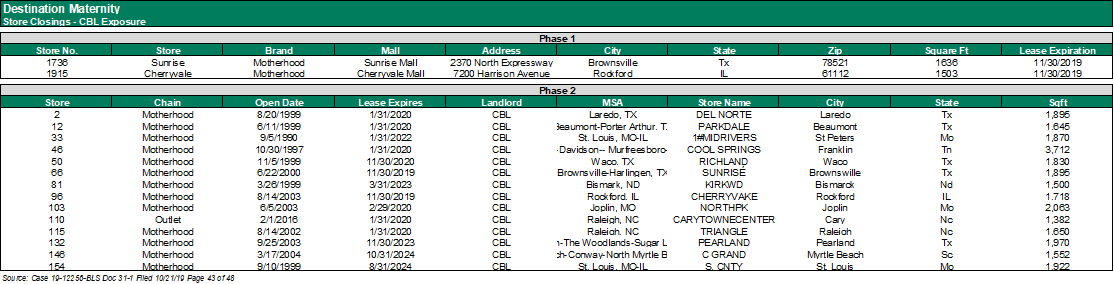

Yesterday, the bankruptcy court granted interim approval authorizing Destination Maternity Corporation ($DEST) to assume a consulting agreement with Gordon Brothers Retail Partners LLC. Gordon Brothers will be tasked with multiple phases of store closures. Among those implicated? CBL, of course:

CBL is landlord to DEST on 16 properties that are slated for rejection. Considering that DEST cops to being party to above-market leases, this ought to result in a real economic hit to CBL as (a) it will lose a high-paying tenant, (b) it will take time to replace those boxes, and (c) it is highly unlikely to obtain tenants at as favorable rents.

Let’s pour one out for CBL, folks. The hits just keep on coming.