🐟New Chapter 11 Bankruptcy & CCAA Filing - Bumble Bee Parent Inc.🐟

Bumble Bee Parent Inc.

November 21, 2019

Tuna fish went from playing a role in the founding of one of the world’s largest private equity firms (Blackstone) to, in the case of Bumble Bee Parent Inc. and its affiliated debtors, another private-equity-backed (Lion Capital LLP) bankruptcy. Bumble Bee is the company behind “shelf-stable seafood” brands Bumble Bee, Brunswick, Sweet Sue, Snow’s Beach Cliff and Wild Selections (as well as a Canadian brand). It has been on a wild ride since 2017.

The bankruptcy narrative is that a plea agreement with the United States Department of Justice related to criminal charges of alleged price-fixing led to burdensome financial obligations by way of (a) a $25mm criminal fine) and (b) defense costs associated with an onslaught of subsequent civil lawsuits from direct and indirect purchasers of products claiming damages arising out of the alleged price-fixing. This overhang ultimately led to the debtors arriving at, but not quite tripping, an event of default with their term lenders in Q4 ‘18. The debtors have been operating under a series of short-term limited waivers ever since as they sought to explore strategic alternatives.

They have one. The debtors have a stalking horse purchase agreement with affiliates of FCF Co. Ltd. “for the sale of substantially all of the Company’s assets at a total implied enterprise value of up to $930.6 million, comprised of $275 million of cash, assumption of the remaining $17 million of the DOJ Fine, and the roll-over of up to $638.6 million in outstanding term loan indebtedness.” This sale will preserve the business as a going concern, preserve jobs, and provide an ongoing business partner to vendors and customers who consider the debtors to be partners.

Debtor first day bankruptcy papers are typically replete with spin and these papers are no different. In fact, necessarily so, they read like an offering memorandum. The papers discuss how the debtors provide “nutricious foods” that are “well-positioned to address a number of important consumer preferences and food trends, including shifts toward protein-rich, low-fat/low-calorie, and high Omega-3 fatty acid diets and trends towards eating multiple small or ‘snack-sized’ portions per day rather than the traditional three-square meals per day, and an overall increase in ‘snacking.’” They have the #1 or #2 market share in the shelf-stable seafood category and 41% of the US share of sales of canned albacore tuna. They also hold “approximately 13% of the U.S. share of sales of canned “light meat” tuna, approximately 12% of the share of sales in tuna pouches, approximately 71% of the U.S. share of sales in ready-to-eat tuna meals, approximately 40% of the U.S. share of sales in sardines, and approximately 16% of the U.S. share of sales in salmon.” It helps that they’re sold at virtually every major bigbox retailer, wholesale club, and grocery store. In 2018, the company had net sales of approximately $933m and adjusted EBITDA of $112.3m and the debtors’ U.S.-based operations contributed $722.2m of net sales and adjusted EBITDA of $86.3m. This is big business.

Putting aside its recent brush with the law, it also faces big market challenges. Questions persist about the safety and viability of shelf-stable seafood, particularly tuna. Indeed, there are headwinds. One sign of this may be that the Company’s overall Adjusted EBITDA has declined by approximately 20% from 2015 to 2018. We assume that, here, the EBITDA is adjusted to ex-out litigation costs.

And then there is this bonkers Wall Street Journal piece noting that consumption of canned tuna has fallen steadily compared with fresh and frozen fish. “Per capita consumption of canned tuna has dropped 42% in the three decades through 2016, according to the latest data available from the U.S. Department of Agriculture. And the downturn has continued, with sales of the fish slumping 4% by volume from 2013 to October 2018, data from market-research firm IRI show.”

This bit is off the charts: “In a country focused on convenience, canned tuna isn’t cutting it with consumers. Many can’t be bothered to open and drain the cans, or fetch utensils and dishes to eat the tuna. “A lot of millennials don’t even own can openers,” said Andy Mecs, vice president of marketing and innovation for Pittsburgh-based StarKist, a subsidiary of South Korea’s Dongwon Group.” To address this trend, the debtors have made forays into the fresh fish category. Otherwise, these challenges will play out another day. With a different owner.

A few more bankruptcy-specific points:

The debtors prevailed over a fee objection by the United States Trustee relating to interim access to $40mm of a proposed $80mm DIP term loan facility and immediate access to a $200mm DIP ABL. It seems that Weil Gotshal & Manges LLP, as counsel to DIP term lender Brookfield Principal Credit LLC had to give the UST a lesson in reverse-Seinfeld Logic. With lending, it is about “taking the reservation” rather than holding or using the reservation: once a debtor obtains a commitment to funds, those funds are committed and technically cannot be allocated elsewhere. The lenders argue, therefore, that fees are warranted upfront.

Critical vendor motions can sometimes be controversial because, naturally, everyone wants to jump the line with critical vendor designation. To get it, however, pursuant to standards set many many years ago, there’s a multi-prong test that must be satisfied. In a nutshell, the critical vendor payments are needed to prevent disruption of a debtors’ business, among other things. Here, the buyer, FCF Co Ltd., seeks critical vendor status to the tune of $51mm (out of a $77mm critical vendor ask). Some other creditors were like “Mmmmmm???” and insisted that the Judge postpone any interim payments until an official committee of unsecured creditors could be appointed. Despite protests from FCF’s counsel, Weil for the DIP lender, and the debtors, Judge Silverstein declined to rule on the motion at the hearing, highlighting the unusual nature of a prospective buyer seeking status. If they want the business, will they really walk away?

Despite these first day fireworks, this should be a relatively smooth one.

One last question it poses is this: will this be just the first of a clump of tuna-related bankruptcies? 🤔

Jurisdiction: D. of Delaware (Judge Silverstein)

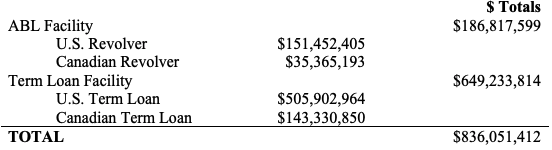

Capital Structure: see below.

Professionals:

Legal: Paul Weiss Rifkind Wharton & Garrison LLP (Alan Kornberg, Kelly Cornish, Claudia Tobler, Christopher Hopkins, Rich Ramirez, Aidan Synnot) & (local) Young Conaway Stargatt & Taylor LLP (Pauline Morgan, Ryan Bartley, Ashley Jacobs, Elizabeth Justison, Jared Kochenash)

Board of Directors: Scott Vogel, Steve Panagos

Financial Advisor: AlixPartners LLP

Investment Banker: Houlihan Lokey Inc.

Claims Agent: Prime Clerk LLC (*click on the link above for free docket access)

Other Parties in Interest:

ABL Agent & DIP Agent: Wells Fargo Capital Finance LLC

Legal: Paul Hastings LLP (Andrew Tenzer, Michael Comerford, Peter Burke) & Womble Bond Dickinson US LLP (Matthew Ward, Morgan Patterson)

Term Loan Agent & Term Loan DIP Agent: Brookfield Principal Credit LLC

Legal: Weil Gotshal & Manges LLP (Matthew Barr, David Griffiths, Debora Hoehne, Yehudah Buchweitz) & Richards Layton & Finger PA (Paul Heath, Zachary Shapiro, Brendan Schlauch)